On Monday, the stock market continued its positive momentum, with the Nasdaq Composite achieving its longest winning streak since January. The S&P 500 and Dow Jones also edged up, with the market pausing to digest the previous week’s robust rally. Investors are eagerly awaiting the Federal Reserve’s announcements and corporate earnings reports for potential bullish catalysts. Additionally, the currency market saw some notable movements, with the EUR/USD, USD/JPY, and other currencies responding to Treasury yields and economic data. As November traditionally performs well for the stock market, investors are keeping a close watch on market developments and central bank policies.

Stock Market Updates

On Monday, the stock market continued its positive momentum, building on last week’s strong rally. The Nasdaq Composite recorded its longest winning streak since January, rising by 0.3% to close at 13,518.78, while the S&P 500 edged up by 0.18% to finish at 4,365.98. The Dow Jones Industrial Average also inched up 0.1% to settle at 34,095.86. According to Adam Sarhan, CEO of 50 Park Investments, the market appeared to be taking a pause to digest the previous week’s robust rally and was waiting for the next bullish catalyst, which could come from the Federal Reserve’s announcements or corporate earnings reports. Notably, Nvidia saw a 1.7% increase in its stock price due to optimism from Bank of America ahead of its earnings report, while Bumble’s shares dropped 4.4% following the announcement that its CEO would step down in January. Meanwhile, SolarEdge Technologies saw a 5.1% decline after a downgrade from Wells Fargo. Bond yields reversed their trend from the previous week, with the 10-year Treasury yield rising by 9 basis points to approximately 4.653%.

The stock market’s recent performance marked the best week of 2023, with the Dow recording its largest weekly gain since October 2022, and the S&P and Nasdaq achieving their best weekly results since November 2022. A softer monthly jobs report had driven bond yields lower, providing support to equities. As the week progressed, there was a lighter schedule for economic data and company earnings, but seasonal tailwinds were expected to bolster the stock market’s recovery. November traditionally performs well for the S&P, and it marks the beginning of the best six-month return period for the market since 1950. The average return for the S&P has been 7% from November through April during this period. Earnings season was also winding down, with over 400 S&P companies having already reported their quarterly financial results. Investors were looking forward to updates from companies such as Walt Disney, Wynn, MGM Resorts, and Occidental Petroleum. Additionally, market participants were closely watching Federal Reserve Chair Jerome Powell’s scheduled speeches, hoping for insights into the potential direction of the central bank’s monetary policy, given the recent trend of lower bond yields.

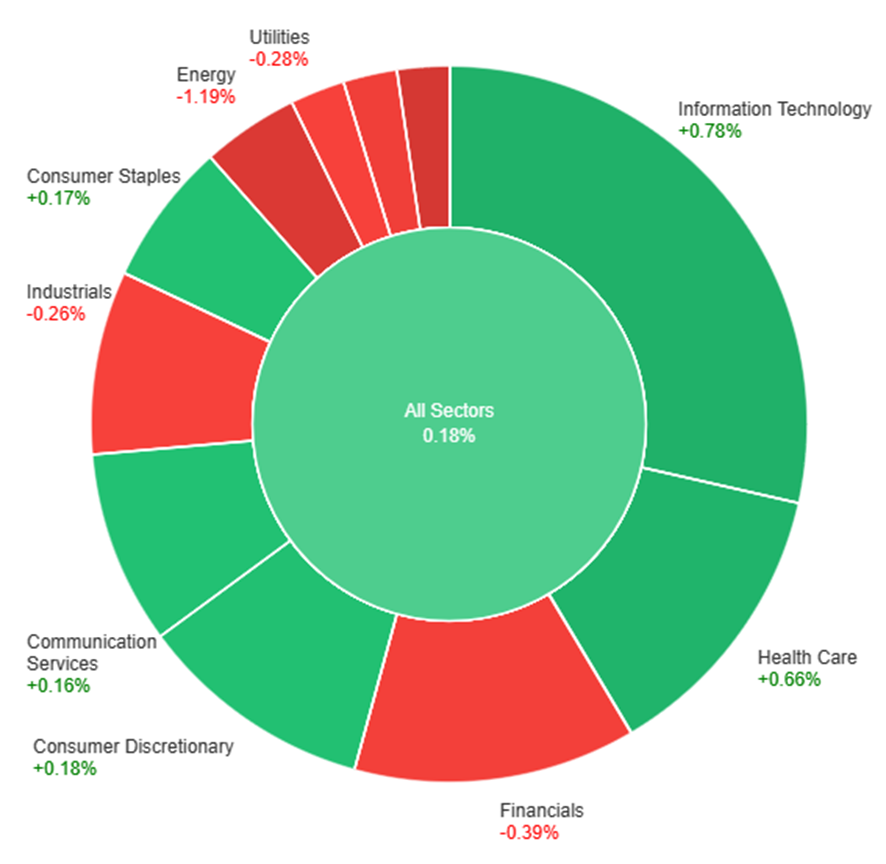

On Monday, the overall market showed a slight gain of 0.18%. Among the sectors, Information Technology and Health Care performed the best, with gains of 0.78% and 0.66%, respectively. The Consumer Discretionary and Consumer Staples sectors also saw modest increases of 0.18% and 0.17%. On the other hand, the Energy and Real Estate sectors faced significant declines, dropping by 1.19% and 1.41%, respectively. The Industrials and Utilities sectors experienced losses of 0.26% and 0.28%, while Financials and Materials both declined by 0.39% and 0.51%.

Currency Market Updates

In the aftermath of Friday’s disappointing U.S. jobs data release, the U.S. dollar index remained relatively stable on Monday. Modest gains in the Euro to U.S. dollar (EUR/USD) and the British pound, however, were countered by gains in the U.S. dollar to Japanese yen (USD/JPY) pairs, largely driven by the rebound in Treasury yields. Much of the previous week’s decline in Treasury yields and the U.S. dollar was attributed to speculative short positions in the Treasury market being squeezed. This squeeze followed relief over the Treasury refunding announcement, diminishing concerns of imminent Federal Reserve interest rate hikes, and was compounded by the soft employment and ISM non-manufacturing reports released on Friday. As Treasury yields and the U.S. dollar appear to be less vulnerable to further losses, market focus turns to the upcoming $112 billion Treasury refund scheduled for Tuesday to Thursday, as well as speeches by Federal Reserve officials later in the week, which are expected to caution against overpricing substantial rate cuts in 2024. The U.S. economic calendar for the week is relatively light, with the next significant data point being the November 14th Consumer Price Index (CPI) report. The CPI is anticipated to show modest growth at 0.1% and 0.3% in both overall and core month-on-month figures, which could reinforce the current market expectations for a rate cut by June.

The currency market experienced some notable movements on Monday, with the EUR/USD reaching a high of 1.0756 but facing resistance from Fibonacci levels and the limited continuation of last week’s yield spread between German bunds and U.S. Treasuries. The convergence of the 100-day and 200-day moving averages at 1.0805-6 and the daily cloud top at 1.0799 on Tuesday represent key technical levels to watch. While Friday’s surge above the 55-day moving average was seen as bullish, the U.S. dollar to Japanese yen (USD/JPY) pair rose by 0.33%, fueled by the rebound in Treasury yields, leaving Japanese government bond (JGB) yields relatively unchanged. The trajectory of Treasury yields this week, influenced by supply dynamics and Federal Reserve comments, is a pivotal factor for the USD/JPY pair. Meanwhile, the Bank of Japan’s potential shift away from yield curve control and negative interest rates may receive some guidance from Japan’s wage data scheduled for Tuesday. Higher long-term JGB yields could make holding foreign exchange-hedged Treasury positions less attractive, thereby supporting the Japanese yen. Notably, the USD/JPY’s recent decline from its 2023 peak to last year’s 32-year high at 151.74/94 raises concerns about a significant double-top reversal in the making. Sterling experienced a slight decline on Monday after relinquishing early gains, with its movement capped by the 200-day moving average. On the other hand, higher-beta currencies like the Australian dollar and the Chinese yuan gained 0.3% and 0.42%, respectively.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Faces Headwinds as USD Index Rebounds Amid Uncertainty Over Fed’s Rate-Hike Path

The EUR/USD pair encounters resistance as the USD Index (DXY) rebounds from an eight-week low, fueled by mixed signals from Federal Reserve officials regarding future rate hikes. This shift led to an uptick in US Treasury bond yields and USD short covering. The uncertainty surrounding the Fed’s next policy move has caused investors to speculate that the rate-hiking cycle may be approaching its end, with market pricing indicating a higher chance of a rate cut in June 2024. All eyes are now on Fed Chair Jerome Powell’s upcoming appearances for further guidance.

According to technical analysis, the EUR/USD moved slightly lower on Monday, easing from the upper band of the Bollinger Bands. Currently, the EUR/USD is trading between the upper and middle band, indicating the potential for a slight lower movement to reach the middle band. The Relative Strength Index (RSI) is at 60, signaling that the EUR/USD is back in neutral bias.

Resistance: 1.0765, 1.0835

Support: 1.0693, 1.0615

XAU/USD (4 Hours)

XAU/USD Softens as Positive Market Sentiment Eases Safety Demand

At the beginning of the week, a more optimistic market sentiment diminished the appeal of safe-haven assets, causing Gold (XAU/USD) to trade at around $1,983 per troy ounce with a softer tone. This decline was tempered by the relative absence of the US Dollar in investors’ focus. Despite limited activity in stock markets due to a lack of significant news, Wall Street’s major indexes extended their gains from Friday. This was supported by government bonds and equities, as the United States Nonfarm Payrolls Report and the Federal Reserve’s announcement signaled the end of the monetary tightening cycle. Central banks worldwide also expressed concerns about the impact of tightening on economic growth rather than current inflation levels, contributing to the overall market stability. While this week lacks significant economic events, the upcoming one is expected to bring updates on inflation from major economies, including the United States.

According to technical analysis, XAU/USD moves lower on Monday and is able to reach the lower band of the Bollinger Bands. Presently, the price of gold is moving near the lower band, creating a possibility to push lower. The Relative Strength Index (RSI) is currently at 38, indicating a slight bearish bias for the XAU/USD pair.