The stock market presented a mixed picture as the S&P 500 closed marginally lower and the Dow Jones hit a record high, while the Nasdaq Composite fell. This cautious trading reflects investor anticipation of the Federal Reserve’s decision on interest rates. In corporate news, General Motors and F5 celebrated stock gains post-earnings, contrasting with declines in Whirlpool and JetBlue stocks. The currency market saw the dollar index dip slightly, influenced by U.S. job openings and consumer confidence data. Attention in the currency market remains focused on the Federal Reserve, with reduced expectations of a March rate cut. Upcoming U.S. labor data and global central bank actions are pivotal in shaping market expectations, impacting various currency pairs, including the EUR/USD and USD/JPY.

Stock Market Updates

In the latest stock market update, the S&P 500 closed almost unchanged, with a slight decrease of 0.06%, ending at 4,924.97, as investors awaited the Federal Reserve’s decision on interest rates. The Dow Jones Industrial Average experienced a modest gain, rising by 133.86 points or 0.35% to close at a record 38,467.31, marking its seventh record closure of the year. Meanwhile, the Nasdaq Composite saw a decline, dropping 0.76% to finish at 15,509.90. The focus is on the Federal Open Market Committee’s two-day policy meeting, with the Fed funds futures market indicating a 97% probability of unchanged interest rates. Investors are particularly keen on any potential shifts in the policy statement concluding the meeting.

On the corporate front, General Motors’ shares surged nearly 8% following better-than-expected earnings, while cybersecurity company F5’s stock increased slightly under 1% after a strong financial report. Sanmina, an electronics manufacturer, saw its shares soar over 28% due to impressive earnings per share and promising guidance for the current quarter. In contrast, Whirlpool’s shares fell 6.6% after the company forecasted a disappointing outlook for the full year. JetBlue also experienced a decline of 4.7% after predicting minimal revenue growth in 2024 and rising costs. These developments come ahead of major tech reports from companies like Microsoft and Alphabet. This earnings season has been positive overall, with about 79% of the 144 companies that have reported, or roughly 29% of the index, surpassing Wall Street estimates.

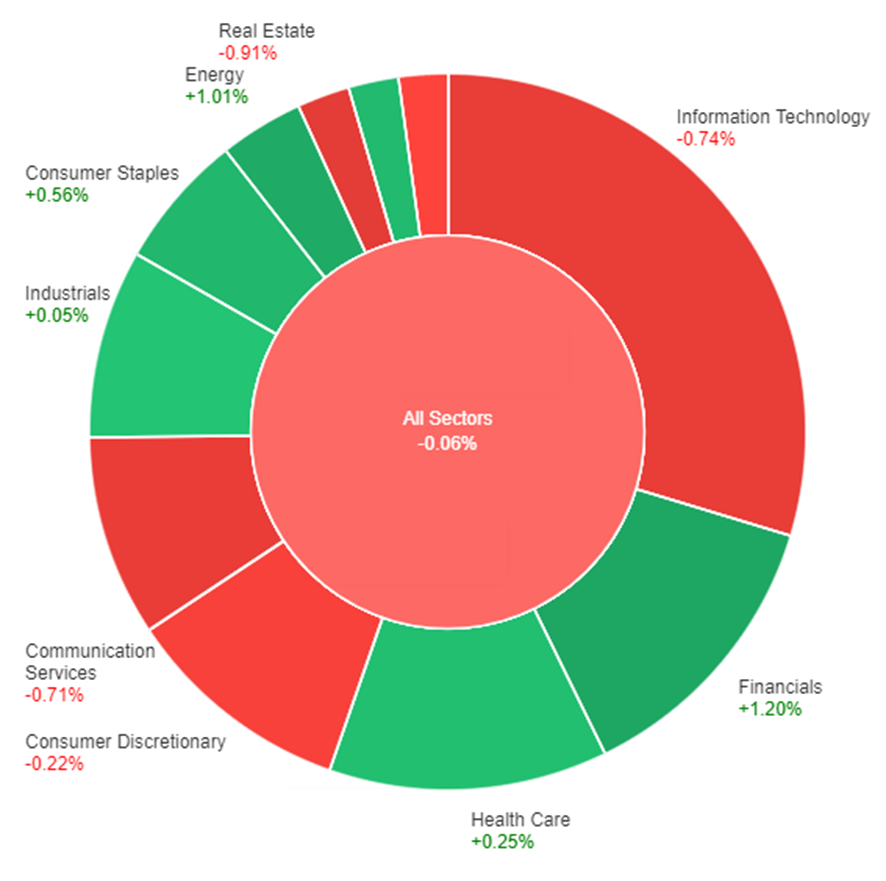

On Tuesday, the overall market experienced a slight decline, with the all-sectors index down by 0.06%. Financials led the gains with a notable increase of 1.20%, followed by Energy and Consumer Staples, which rose by 1.01% and 0.56% respectively. Materials and Health Care sectors also saw modest gains. Industrials barely moved with a slight increase of 0.05%. In contrast, several sectors faced declines, with Real Estate experiencing the most significant drop of 0.91%. Information Technology and Communication Services also struggled, decreasing by 0.74% and 0.71% respectively. Utilities and Consumer Discretionary sectors saw smaller declines. This mixed performance indicates a varied investor sentiment across different sectors.

Currency Market Updates

In recent currency market updates, the dollar index experienced a slight decline of 0.10% during the New York afternoon trade. This movement was influenced by a combination of factors, including month-end selling, stronger-than-expected U.S. job openings, and consumer confidence reaching a two-year high, which met forecasts. Despite these developments, the dollar struggled to maintain its earlier gains, primarily due to concerns arising from the JOLTS data, which indicated an increase in the quits rate alongside higher layoffs and discharges. These factors contributed to a cap on Treasury yields. Regarding the EUR/USD pair, a key component of the dollar index, it remained stable and showed signs of recovery. This rebound followed the pair maintaining support at the 50% Fibonacci retracement level of the October-December rise, marked at 1.0794. Additionally, the Eurozone’s GDP slightly outperformed expectations with a 0.1% increase in Q4, driven by growth in Spain and Italy, although Germany’s GDP results aligned with forecasts, showing a decline.

The currency markets are also closely watching the Federal Reserve’s next moves, with futures markets now indicating a reduced likelihood of a March Fed rate cut, down to 40% from an earlier estimate closer to 50%. This adjustment reflects a market sentiment that aligns more closely with the three rate cuts anticipated in the Fed’s December dot plots. The remainder of this week’s U.S. labor market data, including reports from ADP, jobless claims, Challenger layoffs, and the crucial Friday employment report, will be pivotal in shaping expectations. In the context of the Fed’s favored core PCE inflation gauge falling to the 2% target in the second half of 2023, there is still a significant expectation of a rate cut by March or certainly by May. In comparison, the ECB and BoE are not expected to implement cuts until April and June, respectively, while a modest 10bp hike by the BoJ is anticipated around April or June. In other currency pairs, USD/JPY saw a 0.2% increase following the post-JOLTS rebound in Treasury-JGB yield spreads, while Sterling and the Australian dollar experienced declines amid various economic factors and data releases.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Gains Momentum Amid Mixed Central Bank Signals and Economic Data

Amidst a consolidating US dollar and cautious market sentiment ahead of the Federal Reserve’s FOMC meeting, EUR/USD has shown bullish movements, surpassing 1.0850. The Federal Reserve, expected to maintain its Fed Funds Target Range at 5.25%-5.50%, is facing speculation about delaying a rate cut, possibly shifting from March to May, as recent US economic data indicates a resilient economy. Concurrently, the ECB’s President Lagarde maintains a dovish outlook, emphasizing data dependence and the possibility of a summer rate cut, despite the region’s marginal GDP growth. Contrarily, ECB Board member Centeno surprisingly advocates for earlier rate cuts, supporting economic growth. These mixed signals from central banks, coupled with upcoming US Nonfarm Payrolls data, are contributing to the cautious yet dynamic trading environment for EUR/USD.

On Tuesday, the EUR/USD moved slightly higher, able to reach the middle band of the Bollinger Bands. Currently, the price moving lower near the lower band, suggesting a potential downward movement to reach the lower band. Notably, the Relative Strength Index (RSI) maintains its position at 40, signaling a neutral but bearish outlook for this currency pair.

Resistance: 1.0890, 1.0954

Support: 1.0814, 1.0745

XAU/USD (4 Hours)

XAU/USD Retreats Amid Strengthening US Dollar and Mixed Economic Signals

In the American session, Gold (XAU/USD) witnessed a retreat from its weekly peak of $2,048.64, influenced by the strengthening US Dollar following the release of upbeat US economic data. The surge in job openings to 9.02 million in December, as reported by the US Bureau of Labor Statistics, and a significant rise in Consumer Sentiment to a two-year high, contributed to the dollar’s appreciation. Despite a decrease in government bond yields and the US Treasury’s lowered borrowing estimate for the first quarter of 2024, Wall Street showed mixed performance. The market’s focus remains on the upcoming Federal Reserve monetary policy decision, with expectations of maintained interest rates but a keen interest in potential future rate cuts, as hinted in the Fed’s latest projections.

On Tuesday, XAU/USD moved higher and was able to reach the upper band of the Bollinger Bands. Currently, the price moving lower between the middle band and the upper band suggesting a potential downward movement to reach above the middle band. The Relative Strength Index (RSI) stands at 54, signaling a neutral outlook for this pair.